Skidaway Island Republican Club

President’s Day Dinner

( note: actually a day AFTER President’s Day)

Tuesday, February 21, 2017 Plantation Club

Member Bar: 5:30 PM Dinner 7:00 PM

(Seating : 6:40 pm)

Our special guest speaker is The Honorable Elliott Abrams

"An Early Read/Forecast on The Trump Administration and the Current Status in the Middle East"

Elliott Abrams (born January 24, 1948) is a former American diplomat, lawyer and political scientist who served in foreign policy positions for U.S. Presidents, Ronald Reagan and George W. Bush. He is currently a senior fellow for Middle Eastern studies at the Council on Foreign Relations. Additionally, Abrams holds positions on the Committee for Peace and Security in the Gulf (CPSG), Center for Security Policy & National Secretary Advisory Council, Committee for a Free Lebanon, and the Project for the New American Century. Abrams teaches foreign policy at Georgetown University as well as maintaining a CFR blog called "Pressure Points" about the U.S. foreign policy and human rights.

Cost is $125 per person

Checks to: SIRC – latest February 10\

Coat and Tie requested

Tables available of 10 or 12 or we will match you

Reservations required

Contact: Dick Miller

16 Marsh Tower Lane (598-5049)

hrmatthelandings @gmail.com++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

I will always have a thing about Jane Fonda. This was sent to me and obviously is old and been around but I am re-posting. (See 1 below.)

===

Iran, billions and lies. (See 2 and 2a below.)

===

The Wall Street Journal takes Trump to task regarding his attitude about Putin and throws down the gauntlet.

Trump may play golf, he may even shoot par but trusting Putin is that stretching things too far?(See 3 below.)

+++

Mauldin and his thoughts about 2017. Long but worth reading. (See 4 below.)

+++

Dick

++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++1) Jane Fonda was on TV 3 times this week talking about her new book... and how good she feels in her 70's... She still does not know what she did wrong... Her book just may not make the bestseller list if more people knew.

Barbara Walters said: Thank you all. Many died in Vietnam for our freedoms. I did not like Jane Fonda then and I don't like her now. She can lead her present life the way she wants and perhaps SHE can forget the past, but we DO NOT have to stand by without comment and see her "honored" as a "Woman of the Century." (I remember this well.)

For those who served and/ or died... NEVER FORGIVE A TRAITOR. SHE REALLY WAS A TRAITOR!! And now President Obama wants to honor her!!!!

In Memory of Lt. C. Thomsen Wieland, who spent 100 days at the Hanoi Hilton [infamous North Vietnam prison] --

This is for all the kids born in the 70's and after who do not remember, and didn't have to bear the burden that our fathers, mothers and older brothers and sisters had to bear. Jane Fonda is being honored as one of the "100 Women of the Century."

Barbara Walters writes: Unfortunately, many have forgotten and still countless others have never known how Ms. Fonda betrayed not only the idea of our country, but specific men who served and sacrificed during the Vietnam War. The first part of this is from an F-4E pilot. The pilot's name is Jerry Driscoll, a River Rat. In 1968, the former Commandant of the USAF Survival School was a POW in Ho Lo Prison, the " Hanoi Hilton."

Dragged from a stinking cesspit of a cell, cleaned, fed, and dressed in clean PJ's, he was ordered to describe for a visiting American "peace activist" the "lenient and humane treatment" he'd received.

He spat at Ms. Fonda, was clubbed, and was dragged away. During the subsequent beating, he fell forward onto the camp commandant 's feet, which sent that officer berserk. In 1978, the Air Force Colonel still suffered from double vision (which permanently ended his flying career) from the Commandant's frenzied application of a wooden baton.

From 1963-65, Col. Larry Carrigan was in the 47FW/DO (F-4E's). He spent 6 years in the " Hanoi Hilton"... the first three of which his family only knew he was "missing in action." His wife lived on faith that he was still alive. His group, too, got the cleaned-up, fed and clothed routine in preparation for a "peace delegation" visit.

They, however, had time and devised a plan to get word to the world that they were alive and still survived. Each man secreted a tiny piece of paper, with his Social Security Number on it, in the palm of his hand. When paraded before Ms. Fonda and a cameraman, she walked the line, shaking each man's hand and asking little encouraging snippets like: "Aren't you sorry you bombed babies?" and "Are you grateful for the humane treatment from your benevolent captors?"

Believing this HAD to be an act, they each palmed her their sliver of paper. She took them all without missing a beat... At the end of the line and once the camera stopped rolling, to the shocked disbelief of the POWs, she turned to the officer in charge and handed him all the little pieces of paper...

Three men died from the subsequent beatings. Colonel Carrigan was almost number four but he survived, which is the only reason we know of her actions that day. I was a civilian economic development advisor in Vietnam , and was captured by the North Vietnamese communists in South Vietnam in 1968, and held prisoner for over 5 years.

I spent 27 months in solitary confinement; one year in a cage in Cambodia ; and one year in a 'black box' in Hanoi. My North Vietnamese captors deliberately poisoned and murdered a female missionary, a nurse in a leprosarium in Ban Me Thuot , South Vietnam, whom I buried in the jungle near the Cambodian border. At one time, I weighed only about 90 lbs. (My normal weight is 170 lbs.)

We were Jane Fonda's "war criminals". When Jane Fonda was in Hanoi , I was asked by the camp communist political officer if I would be willing to meet with her. I said yes, for I wanted to tell her about the real treatment we POWs received... and how different it was from the treatment purported by the North Vietnamese, and parroted by her as "humane and lenient." Because of this, I spent three days on a rocky floor on my knees, with my arms outstretched with a large steel weight placed on my hands, and beaten with a bamboo cane.

I had the opportunity to meet with Jane Fonda soon after I was released. I asked her if she would be willing to debate me on TV. She never did answer me.

These first-hand experiences do not exemplify someone who should be honored as part of "100 Years of Great Women." Lest we forget..."100 Years of Great Women" should never include a traitor whose hands are covered with the blood of so many patriots. There are few things I have strong visceral reactions to, but Hanoi Jane's participation in blatant treason, is one of them.

+++++++++++++++++++++++++++++++++++++++++++++++++++++

2) Iran: U.S. Surrendered More Than $10 Billion in Gold, Cash, Assets

Obama admin lowballs cost of dealing with Iran

BY:

The Obama administration has paid Iran more than $10 billion in gold, cash, and other assets since 2013, according to Iranian officials, who disclosed that the White House has been intentionally deflating the total amount paid to the Islamic Republic.

Senior Iranian officials late last week confirmed reports that the total amount of money paid to Iran over the past four years is in excess of $10 billion, a figure that runs counter to official estimates provided by the White House.

The latest disclosure by Iran, which comports with previous claims about the Obama administration obfuscating details about its cash transfers to Iran—including a $1.7 billion cash payment included in a ransom to free Americans—sheds further light on the White House’s back room dealings to bolster Iran’s economy and preserve the Iran nuclear agreement.

Iranian Foreign Ministry spokesman Bahram Ghasemi confirmed last week a recent report in the Wall Street Journal detailing some $10 billion in cash and assets provided to Iran since 2013, when the administration was engaging in sensitive diplomacy with Tehran aimed at securing the nuclear deal.

Ghasemi disclosed that the $10 billion figure just scratches the surface of the total amount given to Iran by the United States over the past several years.

“I will not speak about the precise amount,” Ghasemi was quoted as saying in Persian language reports independently translated for the Washington Free Beacon.

The $10 billion figure is actually a “stingy” estimate, Ghasemi claimed, adding that a combination of cash, gold, and other assets was sent by Washington to Iran’s Central Bank and subsequently “spent.”

“This report is true but the value was higher,” Ghassemi was quoted as saying.

“After the Geneva conference and the resulting agreement, it was decided that $700 million dollars were to be dispensed per month” by the U.S., according to Ghassemi. “In addition to the cash funds which we received, we [also] received our deliveries in gold, bullion, and other things.”

Regional experts who spoke to the Free Beacon about these disclosures said that the $10 billion figure offered by the Obama administration should be viewed “as a conservative estimate for what Iran was paid to stay at the table and negotiate.”

“Iran does have incentives to overstate this figure,” Behnam Ben Taleblu, a research analyst at the Foundation for Defense of Democracies, told the Free Beacon. “But given the recent state-sponsored narrative in Iran about a Western and particularly American failing to offer sanctions relief, this reads much more as fact rather than another instance of disinformation from Tehran.”

It is likely Iran spent a portion of this money to fund its regional terror operations and military enterprise to bolster embattled Syrian President Bashar al Assad, Ben Taleblu said.

“Given the nature of some of this sanctions relief (through the provision of gold and unfrozen assets), this money likely underwrote some of the Islamic Republic’s more destabilizing regional activities,” he explained. “At the macro level, all of this continues to prove one larger point: The way the Iran deal was handled and the provision of sanctions relief during and after the talks that led to the nuclear accord continues to create problems for those interested in defending the integrity of the international financial system.”

One veteran foreign policy insider familiar with the administration’s outreach to Iran told the Free Beacon that the White House has a history of deflating these figures in order to obfuscate details about its contested diplomacy with the Islamic Republic.

U.N. Agency Publishes Secret Iran Deal Docs On Exemptions Obama Admin Dismissed

Top Nuclear Expert: "You just have to ask the question of, what else is being hidden?"

Iran was given secret exemptions allowing the country to exceed restrictions set out by the landmark nuclear deal inked last year, some of which were made public this week by the United Nations nuclear watchdog and others that are likely still being withheld, according to diplomatic sources and a top nuclear expert who spoke to THE WEEKLY STANDARD.

The International Atomic Energy Agency (IAEA) on Friday posted documents revealing that Iran had been given exemptions in January that permit the country to stockpile uranium in excess of the 300 kilogram limit set by the nuclear deal, experts said. The agreements had been kept secret for almost a year, but recent reports indicated that the Trump administration intended to make them public.

TWS reported earlier in December that top Democratic senators also supported releasing the documents.Some details of the exemptions had previously been leaked. The Institute for Science and International Security (ISIS) revealed in September that Iran had been allowed to exceed certain caps in the deal so that the country could come into compliance with the deal's terms.Administration officials dismissed the ISIS report at the time, and surrogates who White House officials have described as the administration's "echo chamber" criticized the organization."The administration was really nasty after we released these documents," David Albright, the founder and president of ISIS, told TWS on Friday. "It was very tough for us to get the information. ... I think that if we hadn't released, they had every intention to keep it secret. They may have given lip service to openness, but I think their intention was to keep it secret."Albright credited the release of the documents as a step towards greater transparency, despite administration attempts to conceal the agreements."You just have to ask the question of, what else is being hidden?" said Albright. "The administration did it to try to minimize the chance that people would know what was in these decisions, and certainly keep those people from talking to people like me in the technical community that can actually interpret what's in those decisions."A source who works with Congress on the Iran issue and who had been briefed on some of the exemptions confirmed that assessment."The Obama team was just hoping to get through the next few weeks without revealing that they've been allowing Iran to go beyond the nuclear deal the whole time," said the source. "That way the president and Secretary of State Kerry could keep declaring that Iran has been following the deal, and their echo chamber could keep saying the nuclear deal is working.""But now it's public. The only reason that the nuclear deal is still in place is because the Obama team has been secretly rewriting to let Iran cheat. The only question is, what's still not being told?"The now-confirmed exemptions reported on by ISIS include allowing Iran to keep low-enriched uranium (LEU) in various forms beyond what's allowed under the nuclear deal. The concession applies to forms that have been "deemed unrecoverable" for use in a nuclear weapon, and Iran has promised not to build a facility to try recover them.That language is not in the nuclear deal, and Obama officials have struggled to defend it. At a State Department press briefing in September after the release of the ISIS report, journalists pressedspokesperso n John Kirby on the decision."You're using this term that's not in the document. I'm just trying to figure out how we can actually check that or understand what it means," said Associated Press reporter Bradley Klapper. "If you say some things are usable but some things aren't, but I don't know which are which, that's not spelled out in the document. That seems to be a new idea here."Albright suggested to TWS that the uranium could actually be recoverable and used in a rush to a nuclear weapon. The State Department in September distorted the nature of the exemption, he said."If this whole thing rests on [Iran] promising not to build a facility that they'd probably only build in secret if they were going to actually break out, then this material probably should not be deemed non-recoverable," he continued. "The State Department … deliberately distorted what was in these decisions to make this point that somehow 'non-recoverable' meant [the LEU] really would never be able to be recovered, regardless if they build a f

++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

3) Bonfire of the Intelligence Vanities

Putin is the winner as Washington melts down over Russian hacking.

What a spectacle. Two weeks before a peaceful democratic transition of power, Democrats are using Russian cyber hacks as an excuse to explain their defeat, and Donald Trump is playing into their hands by refusing to acknowledge that Vladimir Putin is no friend of America. The only winner here is Mr. Putin, who must be laughing at his success in causing Americans to mistrust their own democratic system.

***

The U.S. intelligence community (IC) late Friday finally released a declassified version of the report on Russian hacking that President Obama had requested before he leaves office. The surprise is how thin it is. The report is made up mostly of top-line conclusions, while seven of the 25 pages are devoted to RT, Mr. Putin’s propaganda arm whose anti-Americanism is well known.

The IC report says it couldn’t release details without betraying intelligence sources or methods, but that didn’t stop leakers from whispering some of those details to NBC and the Washington Post. The Post reported that the U.S. overheard Russian officials gloating after Mr. Trump’s victory, saying it would be good for Russian interests. A fair inference is that White House officials authorized those leaks to embarrass Mr. Trump and suggest the election was stolen by the Kremlin.

The report concludes “with high confidence” that Mr. Putin “ordered an influence campaign in 2016 aimed at the US presidential election” to “undermine public faith in the US democratic process, denigrate Secretary [Hillary] Clinton, and harm her electability and potential presidency.” It also concludes that Mr. Putin “developed a clear preference for President-elect Trump.”

Yet the report offers no evidence or judgment that the hacking influenced the election result. The leaks from Clinton aide John Podesta’s email and the Democratic National Committee were embarrassing in their candid views of individuals, but they included no bombshells. The emails that really hurt Mrs. Clinton’s electability were those she kept on a private server while Secretary of State.

American voters were also well aware of the Russian meddling during the campaign, since Democrats made so much of it. “You encouraged espionage against our people,” Mrs. Clinton said to Mr. Trump in the third debate. “You are willing to spout the Putin line, sign up for his wish list, break up NATO, do whatever he wants to do. And that you continue to get help from him because he has a very clear favorite in this race.”

She lost anyway, and for reasons unrelated to the Kremlin. But Democrats and the left want to maintain the stolen-election line because they want to undermine the Republican ability to govern and repeal the Obama agenda that voters rejected at the polls.

As for Mr. Trump, he keeps playing this poorly even by the needs of his own political interests. For weeks he insisted that the Russians may not have done the hacking, though WikiLeaks and Guccifer 2.0 are favorite Russian outlets. He picked needless fights with the intelligence services he will soon need as President. He even cited Julian Assange’s claim that Russia wasn’t the source of WikiLeaks’s campaign dump of Democratic emails, as if Mr. Assange isn’t a practiced liar and deeply anti-American.

The smart line from the beginning would have been to denounce the hack, acknowledge that Russia has been acting in ways that harm the U.S., and say that Mr. Putin should stop or face consequences once Mr. Trump is President. Mr. Trump could also say that if Mr. Obama had retaliated sooner against Russia, the election hacks might not have happened.

Instead, Mr. Trump’s denial of Russian reality makes him look like a sap for Mr. Putin. “Having a good relationship with Russia is a good thing, not a bad thing. Only ‘stupid’ people, or fools, would think that it is bad!” he tweeted on Saturday. He added: “We have enough problems around the world without yet another one. When I am President, Russia will respect us far more than they do now.”

Let’s hope so, but it isn’t “stupid” to mistrust Mr. Putin. After his sheltering of Edward Snowden, his invasion of Ukraine, annexation of Crimea, intervention in Syria, sale of anti-aircraft missiles to Iran and massacre of civilians in Aleppo, only a fool would imagine that Mr. Putin can be trusted beyond the cold logic of military and economic balance of power.

Mr. Trump may be able to build a better relationship with the Russian strongman, but then that’s also what George W. Bush and President Obama thought. Mr. Bush thought his good-old-boy bonhomie could charm him, while Mr. Obama thought the example of his claims to moral superiority would persuade him. Mr. Trump seems to think his advantage will be his superior deal-making skills.

But Mr. Putin respects power, and nothing else. If Mr. Trump wants Russia to respect U.S. interests, he will have to show Mr. Putin that he will pay a price for damaging those interests. This means not covering up nuclear arms-control violations, as Mr. Obama did, and not dismissing or apologizing for Russian cyber attacks, as Mr. Trump has been too close to doing.

***

Mr. Trump won the White House fair and square, and he could help himself by acting like it. The best defense against Russian cyber attacks is to show Americans and the world that he knows better than Mr. Obama how to use U.S. power to deter them. Instead of assailing every critic out of political and personal vanity, it’s time for Mr. Trump to realize that the best revenge against his implacable opponents is to succeed as President.

++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

4) 2017 Forecast: Skeptically Optimistic

By John Mauldin

One might think that all our newfangled technology would make forecasting the future a little easier. I read just last week that scientists have devised electrical wires only three atoms thick. Imagine how powerful a computer chip made with that wiring will be. Yet all our computing horsepower still can’t predict worth a darn what Washington or Wall Street will do to us this year. In fact, there is convincing evidence is that every model that forecasters us is really bad at forecasting, beyond giving us a vague sense of direction.

This is a bigger problem than simply not knowing which way to go. In that situation, you can at least stop and consult your map. Today’s reality is you don’t have a map, and you can’t stop because you are on one of those airport-style moving sidewalks. Unlike the one at the airport, this one has no breaks. You will go all the way to wherever it takes you. Going backwards is not an option, either.

Projecting 2017 is a bit like that. As we’ll see, a great deal will happen in the first third of the year that could (and likely will) radically change the course of events in the last two-thirds. Furthermore, the possible outcomes are in the hands of inherently unpredictable individual humans otherwise known as politicians (and not just in the US, thank you very much!) instead of dispassionate market forces. Fancy quantitative models will be of little help.

Now, don’t take this to mean that I’m pessimistic. I’m not. I ran into Steve Forbes in New York last month, and he asked how I felt about the economy now. I thought for a moment and said, “I’m skeptically optimistic.” He laughed and said that was the perfect answer.

Maybe that’s just another way of repeating the forecast I’ve given you for the last seven years running: My base case is that we will Muddle Through one more year, but with the potential for hitting some serious speed bumps as we round the turn. This is a year to proceed with caution.

Please notice that I’m not saying run for the shelters. I am saying proceed. With caution.

While my answer to Steve may have been perfect at the moment, it omits a lot of detail. So today’s letter will allow me to finish that thought. I’ll tell you both why I’m optimistic and why I’m skeptical.

First, an important announcement. We’ve just opened the registration page for the 14th annual Strategic Investment Conference, which takes place May 22–25 in sunny Orlando. You can save $800 off the walkup rate by registering before Sunday, January 15. But there are only a few of these early-bird tickets. Click here for details.

Our theme this year: “Paradigm Shift: A Deglobalizing World.” Never before have global events weighed so heavily on your investments. That’s why geopolitics will be a focal point on the opening day of SIC 2017. It’s going to be the most exciting SIC yet, and in my humble opinion it will be the single best investment conference of the coming year. To convince you that I’m not just talking the talk, let me walk you through the outstanding lineup of speakers that we have already confirmed.

We have Mark Yusko, the brilliant and witty mind behind Morgan Creek Capital; Gavekal’s Louis Gave, the man you need to listen to on Asian economies and markets; and Dr. Harald Malmgren, whose experience under various US presidents means you’ll definitely want his take on President Trump.

Then there are heavy hitters George Friedman, Ian Bremmer, Raoul Pal, Dr. Pippa Malmgren, Grant Williams, David Zervos, not to mention yours truly, as well as my A-Team, the Mauldin Economics analysts.

Really, we’re only just out of the starting gate. There are many speakers more in the works… including a couple of names I never thought we’d be lucky enough to get. Every speaker at the SIC would headline another conference any day of the week. And because all the speakers know the quality of the lineup, they bring their A games. It’s a race to the top.

My big-picture goal for SIC has always been to create a conference I want to attend. For the last 13 years, that strategy has worked spectacularly. Every year, SIC sells out. And every year, my team gets emails from disappointed readers who didn’t think it would sell out. So there’s my warning, as plain as I can make it. Space is limited. The opportunity to get a ticket at $800 off the walkup rate is even more limited.

I really hope to see you at SIC 2017. Click here to get one of the few remaining early-bird tickets.

I’ll organize this letter around four key themes that I think we will discuss frequently in the next 12 months: US politics, energy, China, and Europe. Then I’ll wrap up with an overarching problem that’s also an opportunity – if we treat it as one.

Let’s begin with good thoughts. Markets have rallied since November on the expectation that Trump and the Republicans will quickly enact a growth-oriented economic agenda, including tax cuts, regulatory relief, and targeted economic stimulus projects. As I talk to people involved in the transition, I am gaining more confidence that a good part of that agenda will actually be realized. It’s clear to me that the right people want it to happen, at least. Whether they will get what they want is a slightly different question.

One reason I’m encouraged is that the Republican majority doesn’t have to start over. They already did some of the heavy lifting in the bills that passed Congress for the last two years, only to see them vetoed by President Obama, and in bills that never got that far because a veto was assured. The Republicans know who does and who doesn’t support these bills. With some minor updating, they can quickly pass the bills again, with a better White House reception this time.

The GOP is also intent on hacking back some of the regulatory tentacles that have impeded progress (and especially job growth) in some industries. They intend to employ a rarely used law called the Congressional Review Act to reverse some of the Obama administration’s regulations. They are also considering legislation that would require federal courts to stop accepting federal agencies’ statutory interpretations and defer to Congress instead.

Tax cuts are almost 100% certain, though their beneficiaries are not certain at all. Constitutionally, all tax bills must originate in the House, and their impact on the deficit will be important to some House Republicans. Passing a tax cut may depend on having a corresponding set of spending cuts ready. Seriously, we simply have no idea how the tax issue is going to play out. Fixing taxes could be problematic: Every dollar the government now spends (or gives in tax benefits) helps somebody, and whoever it is almost certainly has lobbyists on retainer. Nevertheless, we will get a tax cut, though we may not know the nitty-gritty details for a while.

I’m told the Republicans have a long list of relatively uncontroversial (at least on their side of the aisle) bills that they can pass very quickly. They want to show progress, and they think quick passage of some popular measures will buy them credibility to use later. I expect an initial burst of activity after January 20, probably followed by a lull as the Congress moves into more contentious issues like Social Security and healthcare reform. Things will keep happening, but we may not see as many votes.

The hard part is getting agreement on the big items like taxes and healthcare reform. I love seeing Trump and Pence and Ryan and McConnell and all the guys holding hands and acting as if they’re all ready to walk into the bright new future together, but the reality is that there are some quite different ideas in Washington about what serious reforms should look like, and a lot of congressmen want to put their personal stamp on the final bills.

The reform effort could fall apart for various reasons. The Senate majority is narrow enough that just a handful of GOP defectors will be able to stop any given bill, assuming Democrats stay united in opposition. I think Republicans should be on guard against hubris, as well. The decision last week to kick off the year by softening ethics rules was a terrible idea. They accomplished nothing and energized an opposition that was otherwise on its heels. (And I know that many of us are uncomfortable with the concept of a Tweeter-in-Chief, but all it took was one tweet to kill that really bad idea. I mean, Trump stopped it dead in its tracks. Which I believe the vast majority of us will think was a very good thing.)

Finally, as I cautioned last week, there is always the chance that some “bolt from the blue” could change everything. An international crisis, a large bank failure, terror attacks – any one of a long list of unforeseeable events could conceivably derail this train. Not to mention the endemic problems of Europe and China, which we will deal with below and which are entirely foreseeable. But if we can get through the first 100 days with this administration, then I think its agenda will have enough momentum to keep rolling.

Assuming no major surprises, I think the tax and regulation changes can boost GDP growth in the final half of 2017 toward the 2½ percent range. That will be a small improvement from this year and could set the table for a bigger feast in 2018 and beyond. Much also depends on how the Federal Reserve responds, as well as on any changes in its composition.

But here again, if the Republicans get all timid or can’t cooperate and end up settling for the usual tinkering around the edges with tax reform and healthcare reform; and if they are stymied by an entrenched bureaucracy that doesn’t want to see its regulatory powers dismembered, then we can’t expect to get the economic boost that everybody is anticipating. If a policy-driven boost doesn’t materialize, the markets, which have jumped on the anticipation of Real Change, will reverse just as quickly.

That’s why I say, “Proceed with caution.” If my base case plays out and we get reasonable progress on healthcare reform along with regulatory reforms, the stock market could end the year higher, even from today’s elevated valuations; and earnings could really be improving by the third and fourth quarters – if the reforms are actually put into place in time.

If the reforms get hung up or are watered down and not really effective, this market could tumble out of bed so fast that it will make your head spin. I will be saying much more by March about how I think portfolios should be constructed, but my current core portfolio is basically long most of the US market (and long selectively all over the world as well) and has sidestepped the bond market (with some exceptions). All of that could change quite quickly – it’s no surprise to longtime readers that I think portfolios should be actively managed.

That said, passive management will also continue to work if my base-case scenario comes about, and that outcome will just convince more people to move their portfolios to passive management. A market mentor of mine, who had already been trading the markets for 50 years when he began to tutor me, always treated the markets as if they are a personality.

“The market will do whatever it takes to cause the most pain to the most number of people,” was the litany he repeated to me, over and over. The more people that are lured into the grip of passive investing, the greater the pain will ultimately be – which means that this market can go sideways for a lot longer than many of us who have a cautious nature can imagine. We are truly in new territory.

Energy stocks have been tearing higher since the election on bets that the Trump administration will relax environmental restrictions and open more federal lands to oil and gas drilling. Crude oil’s staying north of $50 hasn’t hurt, either. It is up there in part because OPEC threw in the towel and agreed to production limits. Unfortunately for OPEC, those limits don’t apply to US and Canadian shale producers. And the history of OPEC is that they all cheat like crazy.

My friend Art Cashin has an internal “friends and family” list to which he generally sends one or two short, pithy notes per day. For quite some time now, he has been noting the high correlation between the price of oil and the stock market. That correlation is why I have moved my thoughts on energy closer to the front of the letter. The price of energy is important to our portfolios in ways that are not clearly understood but can be observed.

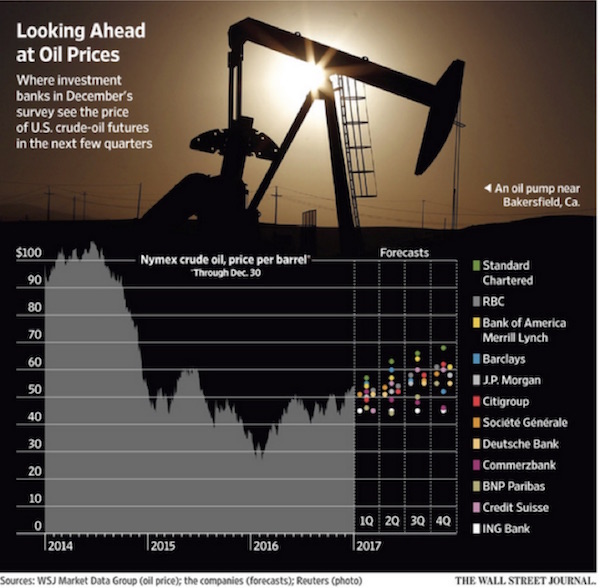

I think it is entirely possible that we will see oil prices climb somewhat further by mid-year, possibly approaching $60, and then pull back as capped US production comes back online. Look at the chart below to see the wide variation among forecasts of major energy analysts working for the big banks.

I also think that this year we’ll start to see a new pattern: Production could keep rising even as prices fall. Conventional wisdom says that producers stop pumping at some point when it becomes unprofitable, but I think that is about to change.

If you are an oil producer – or really, any commodity producer – two things can improve your profit margin: higher selling prices for the resource you produce, or lower production costs. Some combination of both works as well.

Now, selling prices are mostly outside the producer’s control, though adept hedging can help. Cost reduction is therefore the place to concentrate your attention. Back in 2015 I wrote about new drilling techniques and other technology that promised to bring oil and gas production costs significantly lower. Now, in the last few weeks, people in the business have told me these technologies are moving rapidly toward deployment. They foresee considerably lower drilling and production costs by the end of this year.

I had a confidential briefing recently about some new energy production processes that are coming online in the oil patch. Let me just say that production from an oil well drilled with these new techniques is getting ready to increase substantially. In some cases the amount of oil produced per dollar spent on drilling is going to more than double. There are significant chunks of the petroleum-producing parts of the United States where $40 oil will not be a barrier to drilling and new production. Eventually – in a few years – these techniques will begin to show up in wells around the world, and there will be an explosion of oil.

Even as many oilfields dry up, there will be new fields developed from previously unprofitable sources. As I’ve been saying for 15 years, the whole Peak Oil thing is nonsense. I used to think that it simply meant the price of oil would go up to justify the cost of drilling, but I didn’t really understand how much technology would lower the cost of drilling.

This technology trend means that the current oil price range may well break lower, perhaps this year but certainly within this decade, without energy companies losing profits. Not every company will reap the rewards equally, of course; but the industry as a whole is excited. Energy exploration and production is quickly becoming a technology-driven industry, with the US as world leader. If Trump permits construction of more pipelines and natural gas export terminals, we could see North American exports rise considerably in the next few years.

Obviously, over time, a falling energy price will not be good for OPEC or for Russia. Those lower prices will create geopolitical challenges as well as economic ones. I don’t know how it will all shake out. We will likely see some big, energy-driven changes in the world order in the coming decades. But that is beyond the scope of an annual forecast.

Sidebar: every time I write about energy I get the following questions: “What about the environment? Won’t more oil and gas production aggravate climate change?”

Many wonder whether I care about the environment or accept the reality global warming. The simple and very short answer is that I can see the data as well as anyone, and I believe the Earth is in a warming cycle. I very much care about the environment. I don’t want to see the air I breathe or have polluting chemicals in the water I drink. We only get the one Earth, and we have to take care of it.

My full answer is longer and, as you might suspect, more complex. It will end up being a chapter (or a significant part of one) in the book I am writing, called The Age of Transformation. It will be out this year, and hopefully by the time of my conference, if I can at all get it all wrapped up. If you meet me at SIC and we have time for an extended conversation, feel free to ask about these issues. No one-paragraph answers will suffice. Now back to our forecasting.

This is going to be a pivotal year for China. Having to deal with a US president who refuses to play by Beijing’s rules is only part of it, and not necessarily the most important part. China has defied gravity in more ways than I can count. We will see if it can levitate another year or whether it falls back to Earth in 2017. My base case is that they continue the levitation act, but we are going to see an increase in volatility.

I’m not sure how many people are aware that the overnight rate for offshore yuan reached an incredible 105% at one point last week. The Chinese created a massive short squeeze, trying to maintain the value of the yuan. They have spent hundreds of billions of dollars in that effort and are likely to spend more this year.

The natural direction for the yuan, if it were allowed to float, would be significantly lower against the US dollar than it is today. The Chinese are manipulating their currency, but they are manipulating it to maintain its current value and allow it to slowly fall to its natural rate. Any precipitous move in the yuan can unsettle markets quickly.

Further, some $2 trillion worth of Chinese currency has been converted into dollars and moved offshore in the last few years. Think about that in the context of quantitative easing and realize that individual Chinese wanting to move their money out of the country have almost as great an effect on the amount of money sloshing around the developed world as our central banks have. The sources of that money are another subject entirely, but it is enough to note that that money is out in the world, much of it in North America, much of it looking for a home, driving up prices of real estate and other assets.

The Chinese Communist Party will hold its 19th party congress in the fall and will almost certainly give Xi Jinping another five years at the helm. He has become China’s most powerful leader since Deng Xiaoping and could well surpass even Mao before he departs. It could be awhile before he does, too, if this party congress goes according to script.

Xi may need to exercise all his power if he is to maintain both economic growth and domestic order. Sagging exports and rising labor costs are causing manufacturers to turn to automation, but that shift creates unemployment. Xi’s government is doing all it can to keep the masses happy, mostly by handing out generous benefits and subsidies to the usual suspects, including state-owned enterprises. This help makes it very hard to tell which of China’s many state-owned enterprises are actually turning a profit vs. operating at a loss because officials have ordered them to. That is why state ownership is problematic, of course, but for China the alternative may be worse.

A major side effect is that all the stimulus sloshing through an economy with few international exits has nowhere to go. The Chinese have fairly serious limits on the amount of money that individuals can take offshore in a given year. That means there is a lot of money in China looking for a home.

The results are predictable: asset bubbles rolling through regions and asset classes whose valuations follow no discernable logic. These imbalances can’t continue indefinitely, but I don’t know how the Chinese will arrest them. The direct route would be a currency revaluation. That seems to be what they are attempting, albeit very slowly. Ironically, I believe that both Xi and Trump agree they don’t want the yuan to move downward all that much in the coming years.

Xi’s hands are tied: Propping up the value of the yuan is going to force him to use his dollar reserves or to raise interest rates in an already volatile market. The Chinese are getting to a place where manipulation will be a lot more difficult than it has been in the past.

China is trying to do something that would be hard no matter who is in charge. The US is the world’s largest economy because we create most of our own supply and demand. It took us many decades to reach that point; China is trying to do it in about two decades. Their export-heavy model can’t work much longer, but they don’t yet have a way to create sustainable internal demand.

A consumer economy is the opposite of what China has been for the last 30 years of its journey toward becoming a capitalistic society. The export-led model works for the first three stages of national economic development, but it is not what you need to get to and through the last two stages, as I have written in the past. This transition is going to be far more difficult than anything China has faced for a very long time.

Maybe Xi will balance his massive economy perfectly and skip right over the painful adjustments that developing nations (including the US several generations ago) typically go through. I certainly wouldn’t bet against that possibility. The Chinese have been doing things that nobody thought they could do for quite a few decades now. But I won’t bet for it, either, especially this year. All the conditions are in place for major problems in China. That 6.5% GDP growth rate, even if it’s close to correct (and I don’t believe it is), can’t go on forever.

China’s problems are everyone’s problems. I saw a report last week estimating that $1.5 trillion, yes trillion, in corruption proceeds escaped China between 1995 and 2013. That is in addition to the legal money coming out of the country. Most of it landed in the US, Australia, Canada, and the Netherlands, where it has helped to inflate some of our own asset bubbles. In my travels, I constantly run into people who tell me they manage Chinese money. Not trillions, just $50 million or $100 million here and there. It adds up. How much is really out there? I don’t think anyone knows, but it’s a big and growing number.

Our fifty states are essentially what the European Union’s founders wanted: a giant free-trade zone with a currency union and fiscal union. It’s working for us in part because our states, while unique, don’t have the centuries of cultural and linguistic diversity that Europe’s do. I think we underestimate how important our common language and heritage have been to our economic development.

The separate languages, cultures, and histories of its nations don’t mean Europe can’t develop better ways cooperate economically; but the EU structure, specifically the European Monetary Union and the euro, clearly isn’t the answer. I think 2017 will make this fact increasingly obvious to everyone – and possibly undeniable if the worst happens in Italy. Let’s start there.

Italy’s banks are holding something like €350–400 billion in nonperforming loans, depending whose numbers you believe. The vast majority of that amount is not just temporarily NPL; it’s dead money, up in smoke. The banks are pretending otherwise, and the government is letting them. So is the ECB. This is a fact Europe must face. Yet no one wants to face it, and so the leadership is trying to pull off an increasingly ludicrous shell game.

We forget sometimes that banks are themselves borrowers. Most of their lending capital is not equity. They get it by taking deposits and issuing bonds. If a bank can’t collect on the loans it made, it can’t repay the money it has borrowed, and the whole edifice collapses. Bank collapse is ugly, and minimizing the ugliness is one reason we have central banks. We expect our central bankers to remain sober even while everyone else imbibes.

The European Central Bank may be sober, but I’ll bet more that than a few of its member countries would like a drink. Especially in Italy. They are in a near-impossible situation. Huge imbalances exist within the eurozone with no mechanism to resolve them, and Italy is one of the southern-tier countries that is bearing the brunt. That’s not the ECB’s fault. The system was never going to work. Now people are realizing it’s broken, and they are fighting to get out with what they can.

Inflation last month finally reached 1.7% in Germany. You can bet the drumbeat for tighter monetary policy, in place of the all-out massive quantitative easing that we are currently seeing, is going to grow louder in Germany and most of the other northern countries. That is exactly the opposite of what Italy and the southern countries need. See the potential for conflict?

Last week I saw a Spectator article that was not encouraging. I can’t say the following any better than the writer, James Forsythe, did, so I will just quote him.

After the tumult of 2016, Europe could do with a year of calm. It won’t get one. Elections are to be held in four of the six founder members of the European project, and populist Eurosceptic forces are on the march in each one. There will be at least one regime change: François Hollande has accepted that he is too unpopular to run again as French president, and it will be a surprise if he is the only European leader to go. Others might cling on but find their grip on power weakened by populist success.

The spectre of the financial crash still haunts European politics. Money was printed and banks were saved, but the recovery was marked by a great stagnation in living standards, which has led to alienation, dismay and anger. Donald Trump would not have been able to win the Republican nomination, let alone the presidency, without that rage – and the conditions that created Trump’s victory are, if anything, even stronger in Europe.

European voters who looked to the state for protection after the crash soon discovered the helplessness of governments which had ceded control over vast swathes of economic policy to the EU. The second great shock, the wave of global immigration, is also a thornier subject in the EU because nearly all of its members surrendered control over their borders when they signed the Schengen agreement. Those unhappy at this situation often have only new, populist parties to turn to. So most European elections come down to a battle between insurgents and defenders of the existing order.

As James Forsythe says, the conditions that won Donald Trump the presidency exist in Europe as well and are possibly even stronger there. They manifest differently under parliamentary systems, but I see no chance that they will go away. They’re getting stronger, and I think we’ll see proof when France, the Netherlands, and Germany hold national elections this year. It is likely that the Italians will also have to hold snap elections because of the banking crisis, and it is not entirely clear that a majority would support a referendum on remaining in the euro (which is different from remaining in the European Union).

The anti-EU, anti-immigration parties may not win outright control in any of the four countries, but they can still exert enormous influence. These parties may not have the solutions, but the incumbents definitely don’t have them. Given a choice between unlikely and impossible, you have to go with unlikely. That’s what Europeans are doing.

I expect 2017 to bring many changes to Europe, but I’m not convinced it will be the end just yet. “Delay and distract” has worked well for the pro-EU, pro-euro forces ever since the sovereign debt crisis hit in 2010. The europhiles are true believers who simply won’t give up. At some point their determination may not matter, but I suspect they can keep doggedly kicking the can down the road until 2018 or later. It is just not clear when they will run out of road.

When they do, the result will likely be a very severe recession in Europe, which will embroil the world and could push the US into recession if it happens too quickly. Perhaps if we muster the reforms we need here in the US and actually get some sustainable growth going, then a fragmenting Europe might just knock that growth back to the sub-2% or even sub-1% range. But if China, too, loses the narrative in 2017, then all bets are off.

Like it or not, we have entered an era in which machines are learning how to do much of the work that now provides our incomes and, in many cases, our self-worth. This is a topic we will explore in depth in future letters. But a brief summary needs to be interjected here.

The US is manufacturing more materials and goods than ever. Manufacturing is increasing at a fairly serious rate, well over 2% a year. The problem is, manufacturing jobs are not. A Ball State University study calculated that it would take more than 8 million additional jobs to produce what we currently produce today if we were merely at the productivity levels of 15 years ago.

Investment in automation and software has doubled the output per U.S. manufacturing worker over the past two decades. Robots are replacing workers, regardless of trade, at an accelerating pace. “The real robotics revolution is ready to begin” writes BCG and predicts that “the share of tasks that are performed by robots will rise from a global average of around 10% across all manufacturing industries today to around 25% by 2025.” (Source: fortune.com/2016/11/08/china-automation-jobs/)

This is a simplification, but robots and their associated machinery have been somewhere in the neighborhood of four times more important in the loss of manufacturing jobs than off-shoring of jobs has been. But it is hard to protest against increased automation and easier to point a finger at China or Mexico.

The real challenge the US and the rest of the developed world face is how to create new jobs in the face of this automation challenge. The problem is not one we can walk away from. The best estimates that I have read suggest that Korea may be 15–20% more productive than we are in terms of costs, because they are pushing further and faster into the automation process. That trend will leave US manufacturers and exporters – or those in Germany or Italy or any other developed country – behind in the global business contest. Think Japan is not seeing the same thing?

If we don’t automate faster, we lose jobs by being uncompetitive. If we do automate, then we see jobs go away. What we have to do is figure out how to make sure that new jobs are created, and that these jobs are simply not make-work but are rather meaningful and fulfilling. Tall order. For whatever it’s worth, we are programmed in our evolutionary DNA to value what we contribute to the community through our work. Simply getting welfare without a way to eventually make it on your own does not help personal self-esteem or your community.

Incidentally, in the process of writing a book on how the world will change in the next 20 years, with over two dozen chapters on all aspects of the transformation before us, the single biggest and most difficult challenge has been this very topic. One of the reasons the book isn’t finished yet is that I’m still trying to get my head around this very problematic issue. It is at the core of how our society will evolve … or devolve. Not all the paths forward are good ones, and it is critical that we make the right choices.

I gained a new appreciation for the social and political crossroads we are at when I wrote last year about the “Unprotected” voters (to use Peggy Noonan’s term) who flocked to Donald Trump and (to a lesser extent) Bernie Sanders. Both of those men understand that unemployment and underemployment don’t simply reduce people’s incomes, though that’s bad enough. People want to be real contributors to the economy, but the economy increasingly tells them they aren’t necessary.

I’ve been told by people in the transition team that Trump and those around him are laser-focused on restoring jobs and creating new ones, particularly in the Rust Belt states. I have been having more than a few off-the-record conversations with members of the team, and they leave me at least somewhat optimistic that they are thinking about the right problems. It is also clear that they are looking hard for solutions. This is only part of the reason why Trump is pressuring companies to keep jobs in the US. He knows the numbers are small. He’s trying to force a wider change. And the staff around him get this focus.

If Trump succeeds at boosting US jobs, the problem may just be offloaded elsewhere if unemployment rises in Mexico and other places where US companies once operated. We need solutions that bring in the tide and lift all boats at once. Otherwise, conflict will continue and worsen in many different ways and places.

As an economic matter, lower costs and higher productivity are deflationary. Excess supply in the absence of higher demand pushes prices downward. This is why we’ve seen such sluggish growth in the last decade. At some point, faltering growth may turn into outright contraction on a global scale. Then the real problems will begin.

For those of you with some classical economics training, it is as simple as the supply-demand lines that we drew in Economics 101. If you push the supply curve to the right, you are going to find that you are in a new price equilibrium. I am really coming to believe that it is this process that has been (at least partially…) responsible for the lack of inflation that we have seen in the past 15 years. I suspect it has a bigger role to play even than interest rates, though I have no real justification other than personal, anecdotal observation to make that point.

At some point this year, we will be talking about why the whole theoretical construct that nearly all economics is founded upon, that of a dynamic equilibrium, is a false premise. The base case for the economy is not equilibrium, no matter how you define it, but rather constant change and near chaos. Part of the reason that dynamic equilibrium models work so well in theory is that we actually have the mathematics to create them. The fact that these models are perpetually wrong should give us a clue that something else is going on for which we don’t have the math or even sufficient fundamental insight.

This discussion will not only bring us back to Hayek but forward to complexity mathematics and information theory, and I believe all three in combination hold a better way to explain the workings of the economy.

Mainstream economics keeps using the same models and theories, or variations on those theories, but some of the underlying premises of Keynes are simply wrong (not everything of course; he was a brilliant man for his times); and nothing built on a foundation of faulty premises is going to allow you to model the economy in any really useful manner. There’s a lot to tackle with this topic, but it will be fun to try to gain some insight together.

Let me warn you, there are no simple solutions or silver bullets. I’m reminded of the old Blackadder skit where the hero is handed a blank sheet of paper and told that it’s the map to where he is going. When he points out that there is nothing on the page, the man says, “Of course, you have to fill it in. Nobody’s been there” (paraphrasing of course).

2017 will certainly allow us to fill in a lot more of our map. But none of us have ever been there. It is my hope that 2017 will be the year when we start to recognize our true potential for abundance and begin adapting to it, in a way that everyone benefits.

Shane and I will be in Washington, DC, for the inauguration. I am on the board of a public company called Ashford Inc., which manages hotel REITS, among other things. We own several hotels in DC, including the Capital Hilton, and our chairman and my good friend, Monty Bennett, decided we would move our board meeting up a few weeks and hold it in Washington during the inauguration. I will get to see a lot of friends and of course will be at the huge Texas inaugural ball, called “Black Tie and Boots,” on Thursday night (if you are there or in DC, let’s meet); and I’m still looking for tickets for an inaugural ball on Friday night.

We will go straight from DC to the Inside ETFs Conference in Hollywood, Florida, January 22–25. If you are in the industry and coming to that conference, make a point to meet with me. Mauldin Solutions (my investment advisor firm) will have a booth, where I will try to hang out some. If you are an independent broker advisor in the area, make a point to come by and see me. I will be making some big announcements at the conference.

Then I'll be speaking at a one-afternoon conference hosted by S&P Dow Jones here in Dallas on February 1. I will then be at the Orlando Money Show February 8–11 at the Omni in Orlando. Registration is free. I am also scheduled to speak at a large hedge fund conference in the Cayman Islands February 14 to 18. Details on the Cayman conference to follow.

Since this is my personal section, let me clarify what I mean by the term skeptically optimistic in the title. I am by nature optimistic, even though some of you may think of me as a perma-bear. Cautious optimism has actually been studied in the academic literature, and as far as investing goes it’s the optimal stance. Some of the things that the new administration wants to do give me cause for optimism; but the last time the Republicans held both the Congress and the presidency, we made a pretty big hash of things. I know that some of the new faces recognize that fact and are determined not to make the same mistakes. I just hope the new mistakes we make are not as bad as the old ones. Yes, there will always be mistakes made. That’s just part of the governing process. It’s an operation actually run by humans, you know. What else could you expect?

That said, there are a few Trump nominees, as I’ve mentioned in previous letters, who make me a tad nervous (well, more than a tad) in regards to economics and trade. And there is nowhere close to a consensus on what tax reform should look like in Congress and with the Trump administration. But the focus on creating jobs that I mentioned above really does give me grounds for optimism.

I was talking with Newt Gingrich last week, which was the fastest 30 minutes I’ve spent this year. Talking with him when you know you have limited time is like drinking through two fire hoses at once. The next time we talk, I really have to have the three most critical questions that I want answered written out in front of me so that we get to those before we tackle all the other interesting things that we really want to talk about.

He made the observation that Trump seems to be approaching the presidency much more like someone approaches being a governor. For a whole host of historical reasons, I find that to be a source of optimism in and of itself. There have been many politicians who were excellent governors of various states and didn’t quite translate that leadership into being US president. Part of their problem was probably the awesome responsibilities and vast undertakings that a president has to be involved in. I am not certain what that means in terms of how Trump manages things when he is in office. The position seems to change every occupant.

By and large, Trump has nominated people who expect to get results and have done so in their professional careers. One of the criticisms that has been leveled at Trump by the mainstream media has been that he is not appointing people with government experience. I think that is actually his point: We need to stop doing things that are not working. I’m not certain how well the new approach will work, but it’s worth a try. So I think the appropriate attitude is to be skeptically optimistic. And as I said at the beginning of the letter: Proceed with caution.

Let me wish you a great 2017. No matter what happens in the political sphere, I am expecting this to be one of the best years ever for me personally. Of course, I say that almost every year at this time. And often, it is. I have a few New Year’s resolutions that I’m really intent upon seeing through. I will be launching a new business, finishing my “magnum opus,” opening a new chapter in my personal life (involving the M word), and working towards being in the best shape of my life. I really am going to get down below 185 pounds this year. It’s going to be busy year, but it will be a great deal of fun. You have a good week, and next week we’ll look at 2017 forecasts from many of my friends.

Your believing the world will be better analyst,

++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

No comments:

Post a Comment