“When America closes its doors, so does everybody else.”

– Jon Huntsman, Jr.

“Globalization and free trade do spur economic growth, and they lead to lower prices on many goods.”

– Robert Reich

As the entire world is painfully aware, it is election year in the United States. I realize the images my non-American friends see may not inspire confidence. Our process is messy in the best of circumstances, and this year we are not at our best.

I have listened to most of the debates. Candidates on both sides of the aisle have made statements that under their presidency such and such a thing would happen. I sometimes wonder where they are getting their advice. Let me be clear: every candidate does this. And yes, some do it more than others. With all the political shooting from the hip that’s going on, I think it might be instructive for us to look at what the leaders, not just of the United States but of the whole world, are facing as they attempt to make decisions today.

I will structure this exercise as an open letter to the presidential candidates, telling them what I think the winner can expect to face in the way of global economic realities on his or her first day in office. These will be highlights, not an in-depth discussion, but I’ve written on these topics extensively over the past year. Let’s jump right in.

An Open Letter to the Next President

Dear Presidential Candidates:

In ten months and four days one of you will wake up as Mr. or Mrs. President. After the fabulous fun of post-inaugural balls (I wonder if I’ll get an invitation after this letter), you will walk into the Oval Office on Saturday, January 22, and launch into your first 90 days in office, during which you will want to deliver on as many of your promises as possible. But instead of shadowboxing with hypothetical futures on a debate stage, you’re going to be up against cold, hard reality.

My suspicion is that six months into your presidency you will begin to wonder why you ever wanted this job, as the gulf deepens and widens between what you wanted to do and what you can do without unintended consequences. To make your job just a little more manageable, what I would like to do is take you around the world and review some of the economic realities faced by our global partners. For many of them, those realities are not pretty. They may be far more limited in what they can do to respond to your proposed agenda than either they or you would like.

We are going to fly, metaphorically speaking, from San Francisco and head west, first to Japan and China, and then on around the world.

A Quick Summary of the Major Problems You Will Be Facing

First, let’s do a quick overflight of the economic problems you will have to deal with in various regions the world.

- Japan

Japan has run up a debt of almost 250% of GDP, and that monumental debt is growing every year. Japan’s deficit stands at nearly 8% of GDP, the equivalent of a $1.2 trillion deficit in the US. The country’s nominal rate of GDP growth has remained almost flat for 25 years, the result of unrelenting deflation. The Japanese 10-year bond market used to be one of the most liquid in the world. Now, if the Bank of Japan is not in the market, there is literally no trading. If the Bank of Japan were not buying bonds, interest rates would rise precipitously; and the government of Japan would be bankrupt in short order.

In order to avoid a deflationary depression, Japan is monetizing not only its deficit but a great deal of its outstanding debt. This move has of course pushed the Japanese yen down against the dollar – by some 40% in the past few years. The problem is that Japan has no choice but to continue down that path.

As an aside, most mainstream US economists (the very economists you will likely turn to for advice) are telling Japan that it needs to do more quantitative easing, not less. The yen is likely to become markedly weaker on your watch; and, frankly, there is very little you can do about it without sending Japan even further into recession/depression. Such an event in Japan would have serious impacts on global growth and trade.

We’ll get into some details below as to what your options are.

- China

Like Japan, China has a massive debt problem. But unlike the people of Japan, the majority of China’s citizens still live in abject poverty. In a distortion of capitalism, China has built massive excess capacity in a number of manufacturing industries and will now be forced to lay off millions of people or plunge even deeper into the debt abyss. There are significant outflows of Chinese currency as wealthier citizens look to get out of a currency they are worried about.

China is at the point in its evolution where it must shift to a consumer-driven economy, though that transition is nearly always tumultuous. In short, Chinese leaders have much less room to maneuver than everyone might wish.

- Australia

As China changes course from a manufacturing powerhouse to a consumer-oriented nation, Australia is seeing its commodities industries suffer. Plus, Australia’s housing market is priced very high by global standards, and people have a large amount of debt attached to their homes. While there are not many direct economic consequences for the United States, Australia has been a reliable ally, and the Aussie economy is going to come under pressure.

- The Middle East

The Middle East is always a nightmare for US presidents, but you are going to inherit some especially nasty problems. The low price of oil is putting immense pressure on national budgets. Some experts expect Saudi Arabia to literally run out of money by the end of your term. Yes, Saudi leaders can and probably will make adjustments, but the new economic restrictions are going to impair their ability to be part of any coalition to bring stability to the region. And the same problem affects most of our smaller but still important allies in the Muslim world.

- Russia

Economically Russia is not as important as Japan, China, or Europe; but geopolitically it certainly is. Russia simply cannot afford to let the oil price remain below $40 or even $50. Any further downturns in the price of oil will put enormous pressure on President Putin. Russia’s developing financial crisis will continue to make that nation ever less predictable.

- Europe

Outside of domestic concerns, Europe is going to demand your greatest focus. During your first term it is likely that Europe will descend into a crisis that will force the EU either to break up or to mutualize and then monetize its debts – which would then trigger enormous volatility in the currency markets. The topic of massive nonperforming loans at Italian banks (~20% of loans) will move to the forefront at the very beginning of your term if not before. This will be a debt crisis much worse than we saw in Greece. Many small and medium-sized German banks also have severe problems. And let’s not forget France and Spain, which are teetering economically and politically. Europe’s economic problems are only going to make the fallout from its immigration crisis worse and severely limit the ability of our allies to join us in a coalition to resolve crises elsewhere in the world. Be thankful Great Britain is not in as dire a shape as Europe is; you may we ll need the Brits on your side.

- The Americas

It is distinctly possible that Canada could roll over into recession during your first term, and low-priced oil is certainly not helping Mexico, either. The peso is down 50% since the middle of 2013. Brazil is a mess. Its currency is also down 50% in less than four years, and there is no reason it couldn’t fall further. Brazil is likely heading into its deepest recession in over 100 years, which will drag down its neighbors.

- The United States

The US economy is growing by less than 2% annually, and there are reasons to think the economy is slowing further, into the 1% range. We have already waded through the third-longest recovery period in history without a recession; and if by chance you manage to avoid a recession during your first term, the current recovery will become the longest recession-free period in American history. Given the worries I have already mentioned concerning the rest of the world and its impact on us, it is likely that you will have to deal with a recession. As part of your transition process you might want to think about what a stimulus package would look like during a recession. Monetary policy is clearly not going to be enough this time, but you can count on this Fed to give you even more monetary stimulus.

A recession will mean that the US fiscal deficit blows out, and deficit hawks are going to be very wary of fiscal stimulus after the last attempt in 2009–10, which produced very little in the way of measurable results. You will have anti-recession options, but they are limited.

By the end of your first term, it is very possible that tax revenues will cover only entitlement spending, the defense budget, and net interest, meaning that any other parts of the budget will have to be borrowed. To avoid that crisis, you will have to implement significant entitlement reforms or a major tax increase. Either option will be painful, needless to say; and unfortunately, the politicians who governed before you generally put off the serious issues that are going to come to the fore on your watch. The possibility of growing our way out of the budgetary problem, which is the usual political answer, is not going to be realistic without significant tax, entitlement, and regulatory reforms, all of which are controversial. Oh, and income inequality and the pressure on jobs will likely worsen without a serious change in course.

And you want this job why?

Japan: A Bug in Search of a Windshield

The problem with Japan is that for 25 years they didn’t manage to deal with their fundamental problems. They tried to use fiscal deficits and spending to lift them out of their economic malaise without also implementing much-needed reforms. Essentially, the Japanese are savers, and they took their savings and put them into government bonds through various retirement programs and other means (insurance, corporations, etc.) And thereby financed a debt that is now upwards of 250% of GDP. They are running anywhere from 7% to 8% of GDP as a deficit, and they are monetizing an equal amount by buying bonds on the open market.

Essentially, the Bank of Japan is the bond market in Japan. Very few bonds are traded except to the Bank of Japan. Without the Bank of Japan’s presence, Japan’s interest rates would skyrocket, and their interest expense would overwhelm their already deficit-ridden budget. Further, without the massive amount of QE the BoJ is doing – which is proportionately larger than anything the Fed or ECB is doing – the Japanese would face a deflationary recession or worse.

In short – as I was already writing six years ago – Japan is now left with only unhappy choices. No politician can willingly stand by and watch the country plunge into a deflationary depression. We need to understand that the BoJ is doing exactly what the Federal Reserve did during our recent financial crisis, except that Japan’s crisis has extended way beyond whatever time frame they had originally envisioned. It now appears that Japan will be practicing QE for a very long time, at least until the Japanese government balances its budget – which it is now projected to do somewhere out beyond 2020 – and the Bank of Japan has brought enough of the outstanding quantity of JGBs (Japanese government bonds) under the protective wing of their balance sheet so that the market can go back to functioning normally.

I repeat, this Japanese policy has been recommended by the very same economists that you’re going to turn to for recommendations on US policy. The overwhelming majority of mainstream economists (think MIT, Princeton, Harvard, Yale, and Berkeley) are Keynesians or neo-Keynesians and believe in the gospel of QE and liberally applied stimulus, and stimulus is the policy recommendation they are going to deliver from on high when we hit our next recession.

This Japanese policy is going to continue to put pressure on the yen. The yen has already dropped from the mid-70s to between 115 and 123 vs. the dollar in recent months – a 50% drop. While it won’t happen overnight, I think it is very possible that the yen could hit 150 during your first term. A falling yen is going to put enormous pressure on US companies that compete with Japan. It is also going to put enormous pressure on China, Korea, Germany, and all other exporting countries. It is unrealistic to think that they will not respond to protect their market shares.

Japan is at the epicenter of the developing currency wars because the Japanese can’t get off the tiger they’re riding. Oh, from time to time, when traders are too aggressively short the yen, the BoJ will enter into the currency markets and perform an operation to remind people that aggression can be costly. One way and another, the ultimate result is going to be a much lower yen, but the hope is that the fall won’t be too precipitous.

My friend David Zervos observed in his recent client letter that central bankers are very aware of the consequences of their actions, and while they all feel that stimulus and easing are important, they don’t really want to get involved in currency wars. Thus, a short-term rapprochement may have been quietly agreed to at the recent G20 meeting in Shanghai. Quoting David:

What Mario did yesterday was to engineer a credit easing without a currency devaluation. And my suspicion is that this was all part of a gentlemen's agreement back at the G20 meeting. Here was what I think happened in Shanghai. The BoJ and ECB proclaimed that they were both going to ease aggressively in March. The PBOC then said, well if you drive the EUR to parity and JPY to 130 with deeper negative rates, we will break the USD peg. And that’s when everyone said, ooohhh not so fast. It was surely well understood by all participants that the August and January CNY moves had destroyed all the hard reflationary work the ECB and BoJ had done since Q4 2014. And a full break in the CNY peg would bring a further nasty and unwieldy tightening in global financial conditions (i.e. our 1998 argument). No one wanted that! Also, it was no doubt widely understood by all those involved that the Chinese (with the peg in place) could not take a significant strengthening in the DXY given their domestic debt and growth situation. [More on the significance of that below – JM.]

So the players in this very complex currency war game all sat down and came up with a simple agreement. The ECB and BoJ would focus purely on the DOMESTIC credit-easing channel. They would not use these highly powerful negative rates (and forward guidance) to lower risk-free real rates, and in turn weaken their currencies. Further, the Fed likely gave assurances that it would not rates, and in turn weaken their currencies. Further, the Fed likely gave assurances that it would not remove accommodation too quickly via rate rises. That would also keep the DXY in check and give the Chinese time to use fiscal policy and structural reforms to manage the unwind of their debt bubble. All that said, I can imagine the Fed is thinking long and hard about ways to focus less on rate rises and more on a domestic credit tightening if conditions warrant further accommodation removal. The exchange-rate externalities which arise from using rates may simply be too problematic given the delicate bilateral “détente” structure between the PBOC and FOMC. That is certainly some food for further thought.

This win-win approach may in fact work for a period of time, but when there is a true debt crisis in Europe, or if China has a serious hiccup, then it will be every central bank (and country) for itself. I wrote four years ago that the latter half of this decade would bring the most serious currency war we have seen in our lifetime. I really am afraid that I’m going to be right, and it will be on your watch, Mr. or Ms. Would-Be President – and please bear in mind that currency and trade wars of the kind that we had during the early ’30s turned a recession into the Great Depression. It’s going to take a lot of work to keep this worst case from happening on your watch.

China: Beneath the Beautiful Façade

Since the 180-degree turnaround engineered by Deng Xiaoping in the 1980s, China has amazed the world. China has built phenomenal cities and made other amazing infrastructure improvements – railroads, airports, highways, dams, and utilities – and has moved 250 million people from medieval poverty into urban life. That is the largest mass migration in the history of the world by an order of magnitude. China has grown into an export powerhouse and has accumulated trillions of dollars in reserves.

A number of presidential candidates have rightly pointed out that China has not exactly leveled the playing field for American companies, and some have complained about currency manipulation. And now China wants to expand into more areas of business and grow even further. Bloomberg tells us:

China is getting into the venture capital business in a big way. A really, really big way. The country’s government-backed venture funds raised about 1.5 trillion yuan ($231 billion) in 2015, tripling the amount under management in a single year to 2.2 trillion yuan ($340 billion), according to data compiled by the consultancy Zero2IPO Group. That’s the biggest pot of money for startups in the world and almost five times the sum raised by other venture firms last year globally, according to London-based consultancy Preqin Ltd.

The Chinese leadership is targeting anything and everything in an effort to keep their domestic growth alive. But will they be any more successful than they have been with their government-funded solar and wind power sectors? They are more likely to produce a few winners and a lot of losers, just like any other venture capital effort in the world. Throwing a lot of money at startups is not necessarily the best way to create viable new businesses. You actually have to have management and processes. Sadly, successful entrepreneurs are not a dime a dozen. You need an environment that fosters them.

Let’s turn to the steel industry. China has built twice the capacity that it needed even in the period of full-on construction growth. That period is subsiding, yet China still has the capacity to produce more steel than the rest of the world combined. To say that this is excess capacity is a severe understatement. Premier Li has talked about the need to eliminate two million jobs in industries with excess capacity (it’s not just steel; there are a lot of similar situations). The Chinese have already eliminated millions of jobs while trying to move people around and keep the growth engines turning over.

How have they managed to keep growing? The growth is debt-fueled. The balance sheet of the Chinese central bank has risen a hundredfold in 20 years. Twenty years ago China had $500 billion of public and private credit. Today it has $30 trillion. There are estimates that China is adding debt at the rate of $6 trillion a year. New loans to businesses were up 73% in January over the prior year. Some estimate that more than 60% of new debt issuance in recent years has been used to pay interest. In less-polite economic circles, that is called Ponzi finance. There are huge state-owned enterprises (SOEs) that have massive excess capacity and debt they can’t pay. We’re talking debt far more massive than China’s reserves.

Chinese leaders recognize they must try to shift their economy from exports and construction to an emphasis on consumer spending. They want to wean their big SOEs away from debt, which means they have to shrink them, but where will the new jobs come from to maintain consumer spending? They have made some headway, but they are a long way from achieving anything close to a balance. In other countries, this transition has always been somewhat wrenching. Thus, the Chinese are throwing massive amounts of money at venture capital and startups, trying to jumpstart a new source of growth. I am sure all of you have friends in Silicon Valley or Austin or other high-tech regions. Ask them how fast you can go from an entrepreneurial idea to a real business that adds a lot of jobs? Without displacing other jobs? It’s not a short-term process.

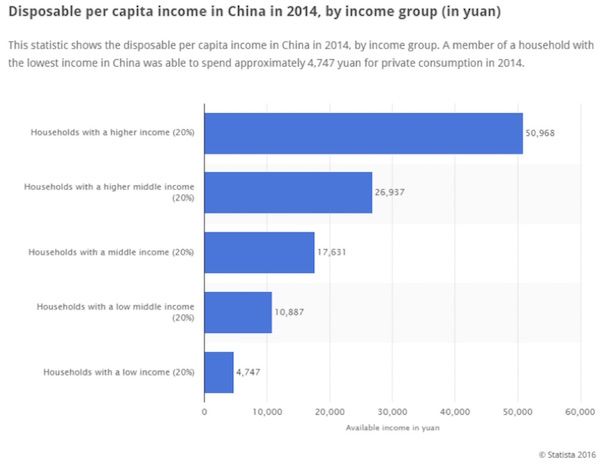

Further, even though we see all the big buildings (and sometimes empty cities), China is a long way from bringing the majority of its citizens anything close to a middle-class living. Look at the chart below from

Statista. The income is shown in Chinese yuan, not dollars. (The yuan is roughly 6.5 to the dollar.)

We see that the bottom 20% of the country, more than 250 million people, is living on disposable income of about two to three dollars a day. The next 20% have roughly twice that. The simple fact is that the majority of the country is still living in fairly abject poverty, with a subsistence lifestyle. Wikipedia documents research that shows upwards of 100,000 protests a year occur in China. There is a great deal of frustration in the country, but the Chinese government is doing as much as it can as fast as it can. This does however create limits on how the Chinese can respond to outside pressures.

For any country in the world, including China, internal pressures and politics will outweigh external pressures.

China has clearly used debt and foreign investments to fuel its growth. It has clearly protected its own industries. And it is coming to the end of its ability to use these means to reliably fuel growth. The new reality constrains China’s policy choices and actions.

And then there is the trade deficit between the US and China. Calculating that deficit is not as straightforward as looking at the bottom-line numbers. For instance, take the Apple iPhone. Its final shipping cost contributes 100% to the Chinese trade deficit, but the iPhone is not made in China; it is

assembled in China. Big difference. Component parts come from literally all over the world in a massive global supply chain. Chinese labor is only a little under $7 of the almost $200 cost. As of a few years ago the countries that were the biggest suppliers of materials for the iPhone were Japan and Germany (

source). Some estimates have the iPhone costing $1500-$2000 if it were made entirely in the United States. Much of that total is due to the very high corporate taxes that Apple would be forced to pay – a cost that would get passed directly to the consumer.

While the iPhone is an extreme example, there are a number of other products that have similar cost structures. Of course, there are many less-complex products that are made wholly in China. Imposing tariffs on Chinese goods would simply add to the cost consumers pay. Candidate Trump’s

proposed 25% tariff on all Chinese goods would result in Walmart shoppers paying that tariff. Unilateral tariffs on products that China is dumping or subsidizing are an entirely different story. We levy such tariffs against a number of countries, especially when we have the ability to manufacture the same products in the US.

Finding a fair, workable balance without creating a trade war is the tricky part. Of course, Chinese theft of intellectual property and engagement in cyber warfare are also factors in the equation. Not easy issues for any president to tackle.

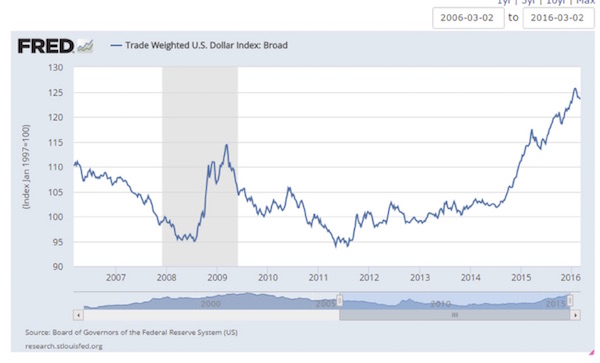

And then there is the matter of currency manipulation by China. China does control its currency, so I guess you can say that’s manipulation, but it is not manipulation in the way some candidates are presenting it. First, let’s look at a graph of the US dollar in a trade-weighted index. Notice that the dollar was markedly weaker from the beginning of the first round of the Fed’s QE until QE began to be phased out. I can tell you that the rest of the world certainly felt that the United States was manipulating its currency, even though technically all we were doing was trying to stimulate the economy.

Now let’s go to a graph of the Chinese yuan over the same 10-year period. Note that the Chinese currency went down against the dollar roughly when we began QE and was allowed to drift further downward until the middle of 2013. Comparing the charts, notice that the dollar began to get stronger a little bit before this period and then began a significant rise. Ninety percent of global currencies (ballpark guess) fell against the dollar during that period. If the Chinese were guilty of manipulation from the middle of 2013 on, they did it by manipulating their currency up, not down.

China now has a currency conundrum. Many of the countries against which China competes for exports have currencies that have fallen significantly against the Chinese yuan. As I noted above in the discussion of Japan, it seems that the G-20 countries have declared a truce in the currency wars. But China cannot allow the euro or the Japanese yen to fall much further against the yuan (and the dollar) without responding. The reason I used the US trade-weighted dollar graph above is that it’s a basket of currencies weighted with respect to those countries we actually trade with. This means it is weighted to Canada and Mexico along with China and Europe. Note that the currencies of some of our trading partners have dropped 50% relative to the dollar!

The Chinese yuan has shown significantly less volatility than the US dollar has in the past 10 years, due to China’s artificially maintaining the strength of the yuan. The problem that the next American president faces is that it is going to be increasingly difficult for the Chinese to maintain that valuation. China is bleeding currency as its wealthier citizens do everything they can to legally move out as much currency as they can.

Now, China’s export industries are suffering from a lack of growth. They are totally reliant upon debt-fueled credit for what growth and debt service they do have.

For many of us, the fact that the Chinese have held it together for this long is rather amazing.

Again, the simple fact is that if China were to fall into recession it would be a major blow to global growth and trade and could even lead to another global recession on the order of 2008, especially if the downturn were accompanied by recession in Europe. Which, as we will see next week, is entirely possible.

The Chinese leadership is constrained by the economic distortions mentioned above. They want to maintain stability and growth, and doing that means they will be limited in their responses to outside pressures. Any negotiation with them, given their constraints, is going to be tough.

We have covered just two major countries, and the letter is already overly long, so I will (hopefully) finish it next week.

Newport Beach, New York, and an SIC Conference Update

I’ll be heading out at the end of month to Rob Arnott’s fabulous advisory council meetings, this time at Pelican Hill in Newport Beach. Those of you who know Rob and Research Affiliates know that his conference is a tad more academic than most, but he combines the intellectual heavy lifting with a fabulous food and party experience. It’s kind of like Adult Nerd Heaven. Then the following week I’ll be in New York, speaking and attending a conference.

For those who want to attend my annual Strategic Investment Conference this May 24–27 in Dallas, I hope you have registered. The conference is sold out, and we are creating a waiting list. We are trying to figure out how to accommodate more people but will not do so if we cannot make sure that the total experience for those already registered will be up to the standards we always strive for.

That said, if you want to attend, I suggest you go to the Strategic Investment Conference

website and register to have your name put on the waiting list. I can almost guarantee that if we do find a way to accommodate a few more folks, those seats will almost immediately disappear, too. Those who wanted to wait to the last month to register are going to be disappointed. I won’t even tease you with the fabulous new speakers that we are seemingly adding every week. It just keeps getting better and better. And since I can’t take everybody to Austin for the amazing local music scene, we are working on bringing Austin music to Dallas. It’s going to be fun! Just a little Texas ambience for y’all.

Most of the family enjoyed a quiet sushi dinner last night to celebrate Tiffani’s 39thbirthday. Somehow, having a 39-year-old daughter makes me feel older than my actual age. And somehow, looking around the table last night, everybody else looked like they hadn’t changed that much in the last 10 years, except for Trey, who is just 21. I look in the mirror and don’t think I’ve changed all that much, either – until of course I look at pictures from 20 and 30 years ago and cringe. But somehow, turning 67 later this year doesn’t seem quite as bad as I think it would have seemed to me 20 or 30 years ago.

We savored our sushi at a wonderful little restaurant called Deep Sushi, which is in an area of town called Deep Ellum. The center of the area is Elm Street, and when the freeways were put in decades ago, the area went downhill and then developed a kind of trendy, counterculture scene … before morphing again to become rather dicey and dangerous. The local merchants hired their own security, and now Deep Ellum is back, bigger and better than ever. Just as in many other cities, there is a growing urban revitalization movement in Dallas (which I am part of because I live in Uptown). Deep Ellum is all of six minutes away from me, with its scores of great eclectic restaurants. It is still very counterculture, and so the majority of people on the street and in the restaurants and bars were young, with plenty of tattoos and long hair and beards. We parked a few blocks away from the restaurant and walked, and my so-called mind kind of flashed back to when I was this yo ung. We thought we were just as cool and every bit as edgy.

In some ways, Dallas is developing neighborhoods much in the same fashion as New York. Downtown Dallas was a ghost town 10 years ago. Now people are buying those ancient skyscrapers and turning them into condos and apartments. Downtown is kind of developing a hip-hop vibe. The street scene is vibrant, with lots of restaurants and stores. Developers are building apartments everywhere around the city center. In the Uptown area where I live, north of downtown Dallas, we are seeing multiple high-rises being built, not to mention massive apartment complexes and retail stores. The food scene is decidedly more upscale here. Then there’s Upper Greenville and Lower Greenville, each with its own distinctive style. All those century-old homes are now being rebuilt. Lakewood, too, has come back. And of course the Park Cities. There are whole neighborhoods within a few blocks of me that are largely Hispanic. A driver and a four iron can get you from here to the gayborhood. A nd the West Village area where I lived a few years ago has a very young, yuppie feel to it.

I kind of like the way Dallas is developing. I’ve always envied New York for its neighborhood environment and being able to walk to food and entertainment. That’s been happening now in Dallas for a decade or two. And don’t look now, but Dallas has become a foodie town. The competition is fierce, but that just means I can find a good meal at a good table.

It’s time to hit the send button, as I have a lot of material to review for the new book. My research groups are beginning to get me their first documents, and I’m still trying to get my own chapters finalized. I knew this would be a massive project, and it is! But at the same time it’s a great deal of fun and intellectually stimulating, so I’m glad I decided to do it. You have a great week.

Your wondering how the elections will turn out analyst,

John Mauldin

=================================================================

No comments:

Post a Comment